Hello everyone.

Today we are going to announce the favorable result of another contradictory expert appraisal.

Hello everyone.

Today we are going to announce the favorable result of another contradictory expert appraisal.

In this case, an industrial warehouse was valued after a sale transaction between individuals and with a declared value of €130,000.00.

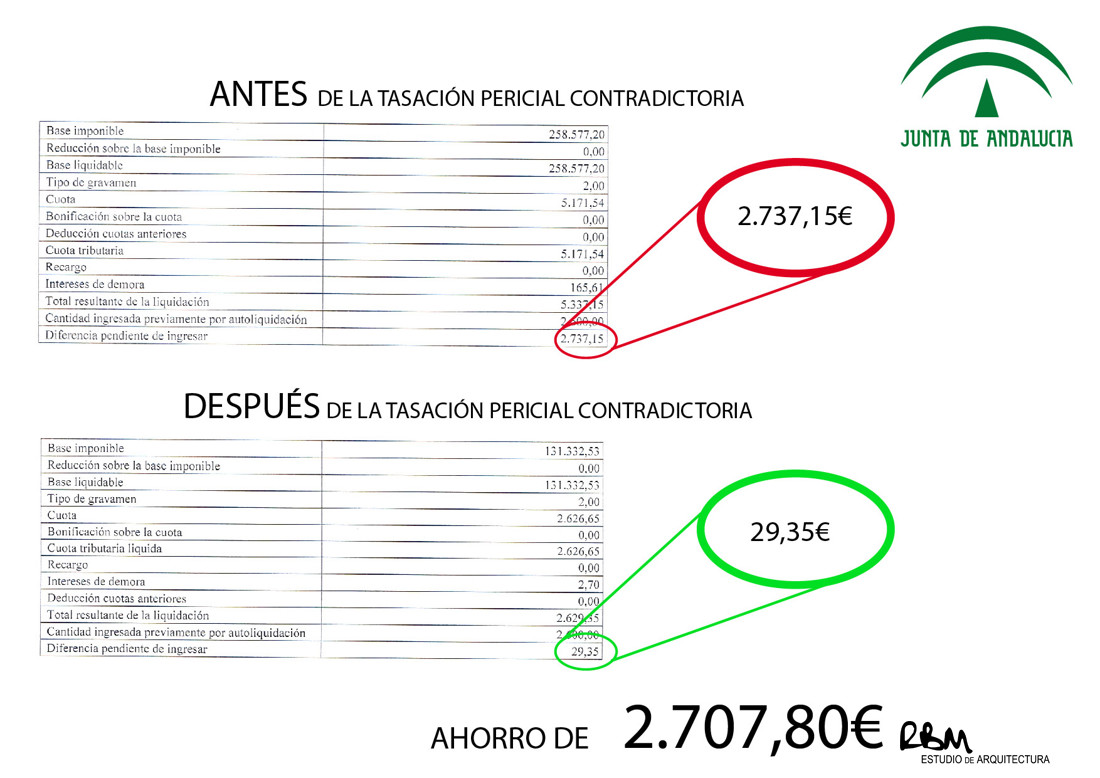

The Administration valued without taking into account the particularities of this building, offering a proven value of €258,577.20.

This verification of values implied an appraisal of almost double the declared value and, therefore, a supplementary settlement of €2,737.15, which was added to the payment of the tax previously made by the buyer (taxpayer).

When the taxpayer did not agree with the value verified by the Administration, he hired me as a part expert to carry out a study of the particularities of the building and provide a reasoned assessment of the building.

This industrial warehouse has two floors, the basement being inaccessible due to a very steep ramp. However, this particularity had not been valued by the administration since the administration expert did not visit the building.

Since the basement was not functional, its value could not be the same as another functional floor. To evaluate it correctly, my criterion was to evaluate the works necessary to make said plant accessible and for this, the demolition of the ramp and the placement of a forklift for vehicles were valued, and then said valuation is subtracted to the value of the plant completely functional.

From that study, I obtained an expert appraisal of €103,271.23.

Since the absolute difference between valuations exceeds 10% of the valuation of an expert of part/witness (Article 135.2 of the General Tax Law), a third expert was used.

The Administration and the taxpayer each deposit the fees of the third-party expert prior to the drafting of the valuation.

The third expert visited the building and detected the same peculiarities that I, as an expert, detected. This was stated in his report and offered a valuation of third expert of €107,306.37, very close to the valuation of part made by me.

Since the valuation of the third-party expert does not exceed 20% of the declared value, the third expert's fees are paid by the Administration (Article 121.8 of Royal Decree 828/1995) and the taxpayer is returned the deposit.

With the definitive assessment, the Liquidating Office issues a new and final supplementary liquidation in which the amount to be paid has been clearly reduced, since the buyer is only asked to pay a supplement of € 29.35 against the sum of €2.737,15 initially estimated.

Therefore, this client has saved more than €2,700.00 in taxes that the Administration wanted to impose unjustifiably, as has been recorded.

In conclusion, the contradictory expert appraisal is a very useful tool for the citizen that, in case of complementary liquidations motivated by incorrect valuations of the Administration for patrimonial transmissions such as the sale, successions or donations, can appeal against the tax collection effort of the Administration.

At RBM Estudio de Arquitectura, we offer to help you in this type of case since we have the experience, the tools and the knowledge necessary to accompany you in the way of contradictory expert appraisals.

A greating.

Raúl Benítez.